I attended a real-estate conference at the Netanya Academic College this week. Its topic was “2013 in review, and predictions for 2014”. A couple of hundred real-estate professionals attended the conference: brokers, lenders, architects, attorneys, contractors, investors, etc. The first half focused on lessons learned from 2013, while the second half focused on predictions for 2014.

During the first half, most speakers were concerned with one topic – housing affordability, or lack thereof. One of the common ways to compare housing affordability is the ratio between ‘average apartment price’ and ‘average salary’. That ratio has been growing rapidly in Israel over the past 5 years, and is approaching 140 ‘salaries per apartment’. The same ratio has been declining within most OECD countries, especially in the aftermath of the 2008 real-estate/finance crisis. By comparison, the same ratio in the US is approaching 55 ‘salaries per apartment’. This means that buying a house in Israel is 2.5x “less affordable” than in the US – certainly a reason for concern.

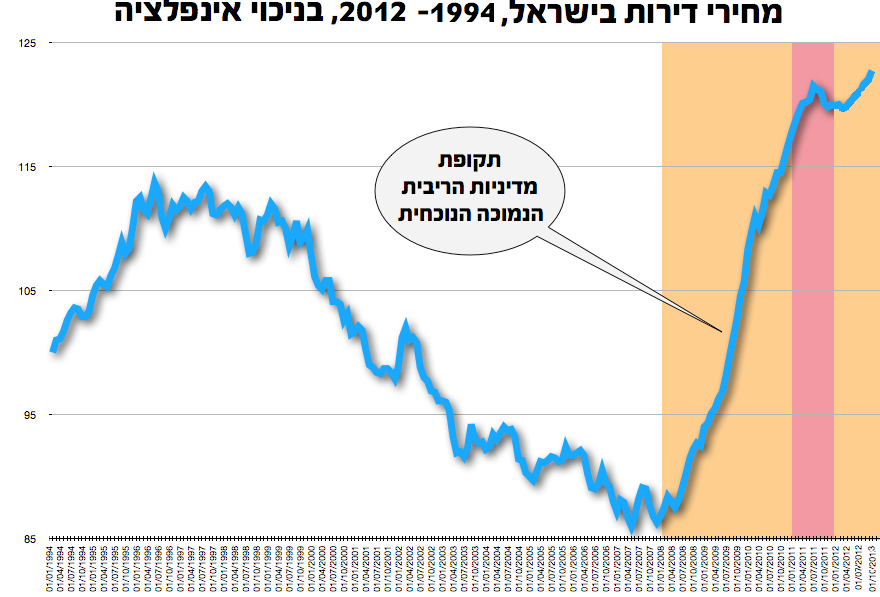

|

| Israel housing prices – sharp increase since 2008 |

The first speaker was former communication minister, Moshe Kahlon. Mr. Kahlon has made a name for himself by leading a sweeping reform in the cellular communication market. He opened the market for competition, and released the Israeli consumer from the suffocating grip of the cellular operators’ cartel. The monthly bill for cellular subscribers dropped by over 50% since, and Mr. Kahlon was touted as the “great defender of the Israeli consumer”.

Mr. Kahlon message was simple: what has been done in the cellular market must be done in the real-estate market. He accused the government of dragging its feet, mainly since it is actually profiting from high real-estate prices (higher price = more taxes). According to him, the process for converting available land into finished apartments is arcane, and extremely lengthy. Due to massive red-tape, it takes on average 13 years from the time the government “auctions” land for construction, till finished apartments are ready for sale. Kahlon also suggested creating regulations and tax incentives for building smaller apartments that fit the needs of younger couples.

|

| Housing prices (green) vs. Wages (red): The gap increases |

Mr. Kahlon speech was full of “truisms” that brought the audience to a standing ovation. Incidentally, there were prior rumors that Mr. Kahlon is about to launch a new political party… The speech gave him great press coverage, on a topic that is near and dear to the general public. His suggestions however reminded me of a favorite quote: “For every complex problem there is an answer that is clear, simple, and wrong”, by H. L. Mencken.

Sure, I agree that real-estate prices are very high in Israel. And I agree that young couples should have access to affordable housing. And it doesn’t make sense that housing in Israel is 2.5x less affordable than in the US. All I am saying is that solving the real-estate problem is far more complex than adding two new cellular operators in order to increase competition…

After a mostly “political” first half, the speakers during the second half tried to focus on “what’s next in 2014”. I particularly liked the presentation given by the head of the college’s finance and banking department. He referenced research done by the Israeli Central Bank about housing prices.

According to that research, over half of the housing price gains are attributed to low interest rates. The rationale was simple: a) low interest rates make bigger mortgages affordable; b) low interest rates drive investors away from bank deposits and government bonds to the real-estate market. In short – both regular households and investors are willing to pay more for housing, while interest rates remain very low.

The other factor that drives real-estate prices is of course supply & demand. However, according to the above research, it accounts for less than 40% of the price increases. Given the economic conditions in the US and Europe, it seems that interest rates will remain extremely low for the foreseeable future. So the only room for maneuver is to try to increase supply and reduce demand…

One of the ways to reduce demand is to levy more taxes, especially on those who buy real-estate for investment purposes. A representative from the Israeli Tax Authority presented the new taxes on “investment property” that took effect in 2014. There was no ‘standing ovation’ after his talk, since many of those present will actually be negatively impacted by those taxes…

Real-estate prices are intricately connected to the overall economy. Another research was quoted, indicating that higher real-estate prices generate a “sense of wealth” among house owners. That confidence drives more personal spending, and therefore an increase in the GDP. It was estimated that over 0.5% of the annual GDP growth is attributed to that “sense of wealth” alone.

There have been, and will continue to be, many suggestions on how to address the “real-estate” bubble in Israel. My hope is that any steps taken will lead to a “soft landing” rather than a bubble burst. My concern is that due to the complexity of the problem, the number of organizations involved, and the politics – engineering a ‘soft-landing’ is next to impossible.

What does a real-estate “bubble burst” look like? We don’t need to look very far. The US has gone through such a process only 5yrs ago. Real-estate prices dropped rapidly, financial institutions came to the verge of collapse, unemployment rapidly rose, and the US went through the worst economic recession since the 1930’s. Not pretty.

Real-estate problems are complex and take years to solve. They require collaboration on the national and local government levels. My hope is that the government will focus on innovative ways to increase housing supply. Yes, it should streamline the planning and building permission process – but without compromising the environment. It should heavily invest in transportation, so that people can live in remote suburbs, yet easily get to work in the metropolitan areas of Tel Aviv, Jerusalem and Haifa.

As for 2014? The bottom line from the conference seems to point to real-state prices continuing to increase. My dream of buying a spacious apartment in Tel-Aviv will probably continue to slide further into the future. Perhaps after the bubble bursts…

We have to follow every rules in decorating our property investment. It really is helpful for our business and also for our Property Investment Portfolio to be stable and successful. Organize our business and make sure that we do market our business well to achieve our dreams.

http://www.positivepropertyinvestments.com.au/property-investment.html

LikeLike

Excellent pieces. Keep writing such kind of info on your page.

Im really impressed by your blog.

Hi there, You’ve done a great job. I’ll certainly digg

it and personally recommend to my friends. I am sure they’ll be benefited

from this site.

LikeLike